English

English

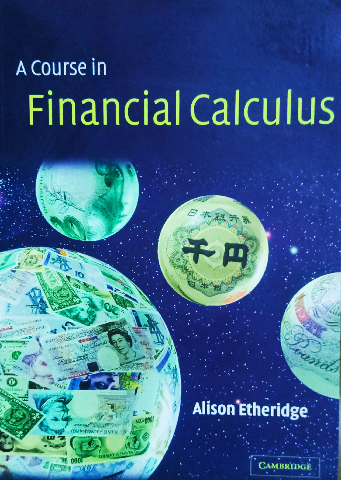

Finance provides a dramatic example of the successful application of advanced mathematical techniques to the practical problem of pricing financial derivatives. This self-contained 2002 text is designed for first courses in financial calculus aimed at students with a good background in mathematics. Key concepts such as martingales and change of measure are introduced in the ,discrete time framework, allowing an. accessible account of Brownian motion and stochastic calculus: proofs in the continuous-time world follow naturally. The Black-Scholes pricing formula is first derived in the simplest financial context. The second half of the book is then devoted to increasing the financial sophistication of the models and instruments.

| Shipping Cost |

|

| Delivery Time | Ready to ship in 3-5 Business Days |

| Shop Location | Cairo, مصر |

No reviews found!

No comments found for this product. Be the first to comment!